Selecting between a Roth IRA and a Conventional IRA in 2026 is without doubt one of the most vital retirement choices for U.S. traders. The account you choose can affect how a lot you pay in taxes over the subsequent a number of many years and the way a lot revenue you retain throughout retirement.

When you’re evaluating Roth IRA vs Conventional IRA within the USA for 2026, this information explains tax variations, contribution limits, revenue guidelines, and which possibility could also be higher primarily based in your monetary scenario.

Fast Comparability: Roth vs Conventional IRA (2026)

Right here’s a simplified overview:

Roth IRA

Contributions made with after-tax {dollars}

Certified withdrawals are tax-free

No Required Minimal Distributions (RMDs)

Earnings limits apply

Conventional IRA

Contributions could also be tax-deductible

Withdrawals taxed as unusual revenue

RMDs start at age 73

No revenue restrict for contributions (deduction limits could apply)

Each accounts can be found by means of main U.S. monetary establishments reminiscent of Constancy Investments, Vanguard, and Charles Schwab.

The true distinction comes right down to taxes.

A Quick Comparison Table:

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax Now | No deduction | Tax deductible |

| Tax Later | Tax-free withdrawals | Taxed withdrawals |

| Income Limits | Yes | No income limit for contributions |

| RMDs | No | Yes |

The Core Distinction: Taxes Now vs Taxes Later

The most important distinction between a Roth IRA and Conventional IRA is once you pay taxes.

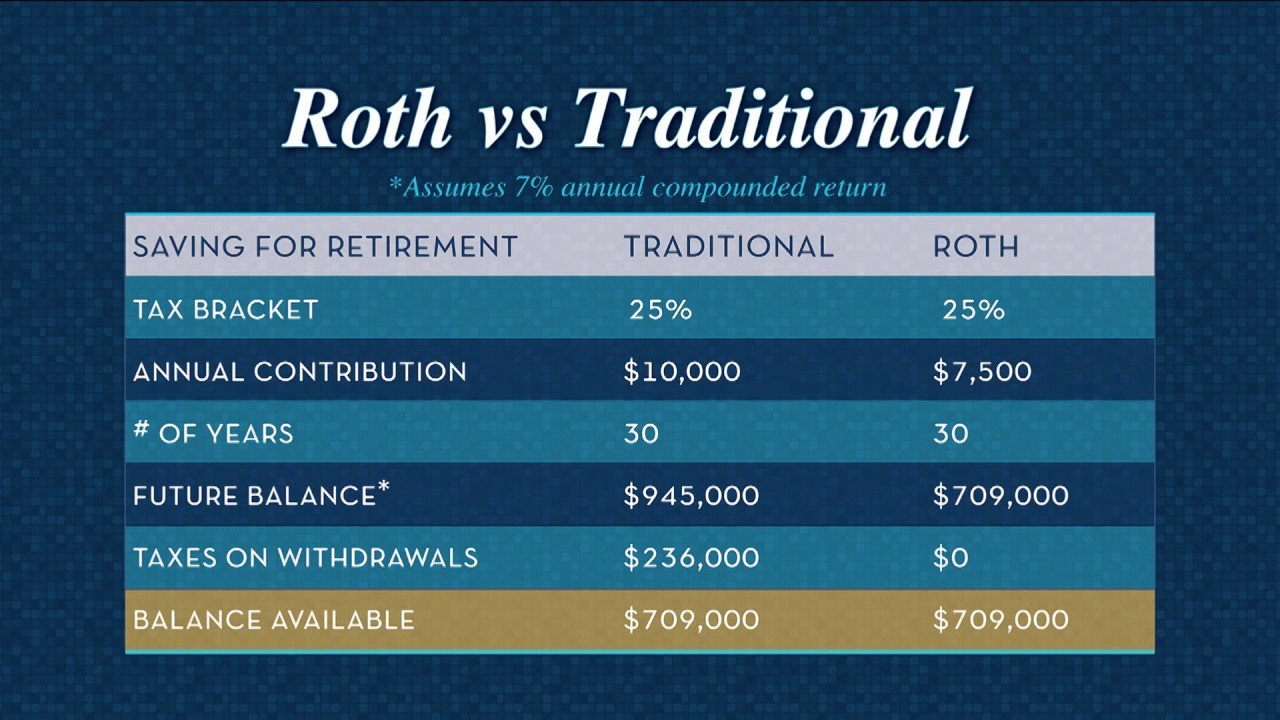

With a Conventional IRA, you could obtain a tax deduction in 2026. This lowers your taxable revenue immediately. Nonetheless, withdrawals in retirement are taxed as common revenue.

With a Roth IRA, you pay taxes upfront. However certified withdrawals in retirement — together with funding beneficial properties — are tax-free.

The important thing query is:

Will your tax price be greater or decrease in retirement?

When you count on greater taxes sooner or later, a Roth IRA could present long-term benefits. When you count on decrease taxes in retirement, a Conventional IRA could supply quick financial savings.

2026 Contribution Limits and Earnings Guidelines

For 2026, IRA contribution limits are anticipated to remain round:

Below age 50: Roughly $7,000 yearly

Age 50 or older: Roughly $8,000 with catch-up contribution

Roth IRA Earnings Limits

Roth IRAs have revenue phase-out limits. Excessive-income earners could not qualify for direct contributions.

In that case, some traders use a backdoor Roth technique, which includes contributing to a Conventional IRA and changing it.

Conventional IRA Deduction Guidelines

There isn’t any revenue restrict to contribute to a Conventional IRA. Nonetheless, in case you are lined by a office retirement plan, your means to deduct contributions could also be restricted primarily based on revenue.

Understanding these guidelines is crucial for optimizing your retirement tax technique in 2026.

Required Minimal Distributions (RMDs)

Conventional IRAs require you to begin taking Required Minimal Distributions at age 73. These withdrawals are taxed and might improve your retirement revenue tax burden.

Roth IRAs don’t require RMDs through the unique proprietor’s lifetime. This supplies extra flexibility in retirement and will help handle taxable revenue extra effectively.

For traders who need management over once they withdraw funds, Roth IRAs supply a transparent benefit.

Which IRA Is Higher Primarily based on Earnings?

Excessive Earnings Earners

In case you are presently in a excessive tax bracket, a Conventional IRA could assist scale back your taxable revenue in 2026. Nonetheless, should you count on to stay in a excessive bracket throughout retirement, Roth methods could present larger long-term tax financial savings.

Many excessive earners diversify by contributing to each account sorts over time.

Center-Earnings Professionals

In case your revenue is predicted to develop sooner or later, a Roth IRA could also be extra helpful. Paying taxes at immediately’s decrease price might lead to vital tax-free revenue later.

Youthful traders usually profit most from long-term tax-free progress.

Close to Retirement (Age 50+)

If retirement is inside 10–15 years, quick tax deductions from a Conventional IRA could also be useful. Nonetheless, Roth IRAs can scale back taxable revenue later and eradicate RMD issues.

The correct alternative usually depends upon your anticipated retirement revenue sources.

Lengthy-Time period Progress Issues

Over many years, tax-free progress could make a considerable distinction.

For instance, contributing persistently for 25–30 years permits funding beneficial properties to compound. With a Roth IRA, these beneficial properties aren’t taxed when withdrawn.

In distinction, Conventional IRA withdrawals are taxed as revenue, which may scale back total retirement spending energy.

Because of this many long-term retirement methods favor not less than partial Roth publicity.

Frequent Errors to Keep away from

Ignoring Roth revenue phase-outs

Overcontributing and triggering IRS penalties

Not planning for RMDs

Failing to diversify tax publicity

Making choices primarily based solely on present taxes

Good retirement planning focuses on lifetime tax effectivity, not simply short-term deductions.

Can You Have Each a Roth and Conventional IRA?

Sure.✔

Many U.S. traders use each accounts to create tax diversification. This technique permits flexibility in retirement:

Withdraw from Roth accounts to keep away from taxes

Withdraw from Conventional accounts when in decrease tax brackets

Having each sorts can present higher management over retirement revenue planning.

Ultimate Verdict: Roth IRA vs Conventional IRA in 2026

Select a Roth IRA if:

You count on greater taxes in retirement

You need tax-free withdrawals

You favor no RMDs

You might be early in your profession

Select a Conventional IRA if:

You want a tax deduction immediately

You count on a decrease tax bracket later

You need to scale back present taxable revenue

For a lot of traders in the US, the simplest technique in 2026 could contain contributing to each account sorts over time.

Backside Line

The choice between a Roth IRA and Conventional IRA in 2026 depends upon your revenue stage, anticipated future tax bracket, and long-term retirement objectives.

Understanding how every account is taxed — immediately and sooner or later — lets you make a extra knowledgeable choice and probably maximize your retirement revenue.

Earlier than opening or contributing to an IRA, overview your present tax scenario, projected retirement revenue, and long-term monetary aims to find out which technique aligns finest along with your objectives.